A strong dollar is good for the American economy. Not only does a strong dollar mean that there is a healthy demand for American-made goods and services, but, perhaps more important, it’s also a show of confidence in the U.S. government and financial institutions.

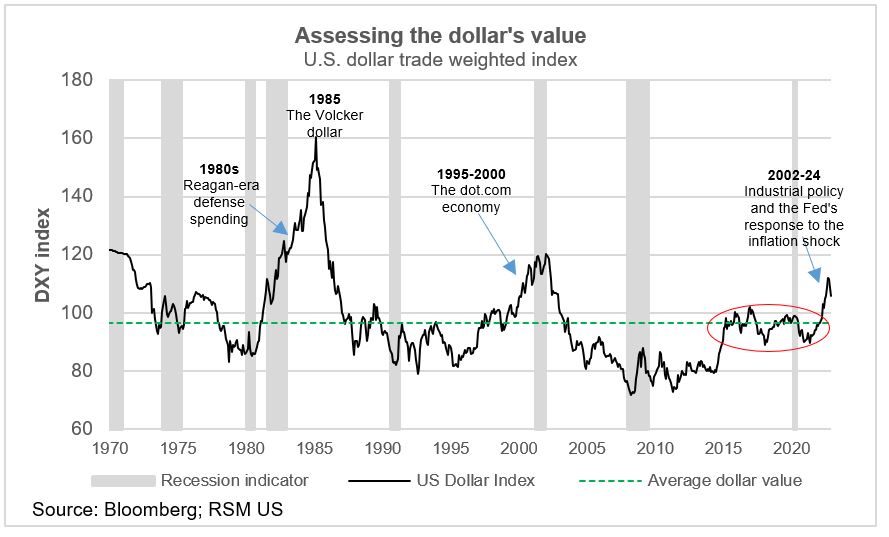

The United States has benefited from a profound shift in global capital flow, which has boosted the dollar.

Like any asset, the dollar’s value is based on its demand. When demand increases, whether for trade purposes or financial transactions, the value increases.

Now, with an economy outperforming its peers, the United States has become a magnet for global investors looking for better returns, a dynamic that will continue even as interest rates ease later this year.

The United States has benefited from a profound shift in global capital flows, mopping up more than 30% of these flows. Before the pandemic, that figure was 18%.

This shift has boosted the dollar, which we think will continue as the global economy adjusts to higher inflation and higher interest rates.

Other factors driving the dollar higher have been trade and spending: the nearshoring of global supply chains; the adoption of industrial policies that nurture nascent technologies; and a rise in American defense spending.

Although policies like these can lead to higher prices for households, they also lead to a stronger dollar, which can dampen those higher prices as imported goods become cheaper.

In the end, the strong dollar is a benefit for the America’s real economy. As Robert Rubin, the U.S. Treasury secretary in the 1990s, famously said, “A strong dollar is in our national interest.” We think we are in a similar time.

The state of play

On a nominal non-trade-weighted basis, the dollar increased in value against 14 of the major 16 trading currencies as of July 10, including 3% gains against the euro and the pound, nearly 5% against the Canadian dollar and approximately 33% against the yen.

On a trade-weighted basis, the currencies of our major trading partners in the West—the euro, Swiss franc, Japanese yen, Canadian dollar, British pound and Swedish krona—are all down against the greenback, with the euro accounting for more than half of the index.

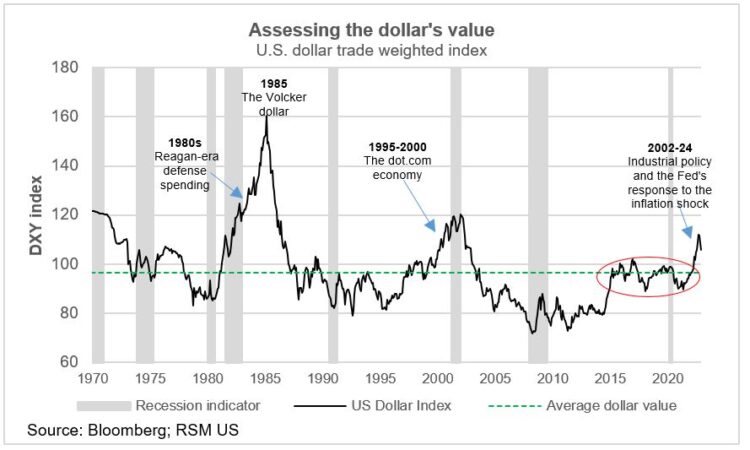

It is no coincidence that the dollar is at its highest level since the dot.com economy of the late-1990s.

Despite threats of the trade war, the pandemic and the standoffs in Congress over funding the government, the dollar has been resurgent, a rise we attribute to the strength and innovation of its economy and to the re-establishment of U.S. leadership in global affairs.

It is no coincidence that the major U.S. trading partners included in the dollar index also happen to be the major international financial centers.

And it is the increased demand for U.S. long-term securities from those centers that speaks most to the enduring strength of the dollar. Anyone can invest in the safety of a Treasury bond or U.S. investment-grade corporate bonds.

It is important to note that international investment became efficient and profitable only after President Nixon floated the dollar in 1973. Ending the gold standard created the currency markets we have today, which facilitated the growth of international investment and the economies of the Western world.

As it turned out, foreign demand for long-term U.S. securities took off in the late-1990s when American based technological innovation begin to drive the structural transformation of the domestic and global economies.

Everyone wanted a piece of the action.

And then as the global supply-chain became viable, the transaction demand for dollars and short-term dollar-denominated securities increased along with the increase in commerce conducted in dollars.

Apart from the commercial demand for short-term U.S. securities used by exporters to park their receipts before reshoring the funds, we can see the current value of the dollar boosted by foreign demand for U.S. long-term securities. Net flows into U.S. securities are at levels reached only before the 2008-09 financial crisis.

Continued dollar strength

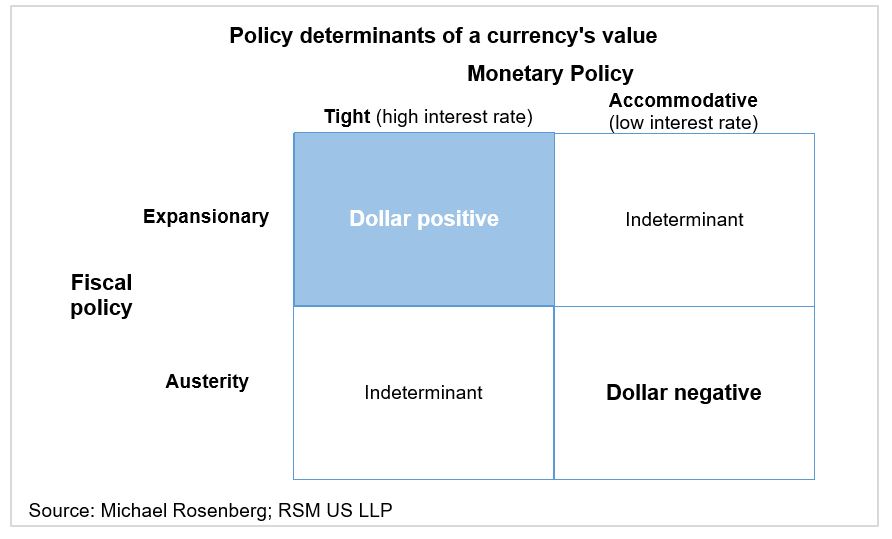

A tight monetary policy (high interest rates) and an expansionary fiscal policy (government spending) are associated with a stronger currency.

At the opposite end, a combination of an accommodative monetary policy (low interest rates) and fiscal austerity is a prescription for a weaker currency.

The present circumstance, which include a still tight monetary policy and a fiscal tailwind, have set the stage for continued dollar strength.

Financial-based strength

On the financial side, the dollar is benefitting from the attractiveness of U.S. equity market, in particular the U.S. technology sector, and the safety of the Treasury and corporate bond market that underpins all investment.

On average, Treasury notes have yielded 185 basis points more than German bunds since 2016, with diverging trends in monetary and fiscal policies and economic growth expected to continue.

U.S. high-grade corporate bonds offer another 150 basis-point pickup over Treasury securities and have become that much more attractive to foreign investors.

The European Central Bank has already started lowering its overnight policy rate in response to the region’s flat economic growth, particularly in Germany.

That presents the case for an accommodative monetary policy on the continent. And the central banks in Canada, Sweden and Switzerland have already begun cutting their policy rates, with the Bank of England likely to cut its base rate as early as next month.

At the same time, the U.S. economy and labor market are engaged in a period of sustained growth, with the Federal Reserve waiting for further confirmation that inflation has been subdued.

With the likelihood of the Fed’s first policy rate cut now delayed until the fall, and assuming an orderly and gradual lowering of the federal funds rate, that suggests that U.S. interest rates will remain high compared with counterparts in the West.

A fiscal tailwind

The dollar’s continued interest-rate advantage is one half the prescription for dollar strength. The other half of the equation, or the fiscal half, is already in place.

The U.S. economy and the dollar have weathered anything thrown at them, especially compared with major trading partners.

Canada’s unemployment rate, for example, has moved back up while inflation in Europe and the U.K. has dropped precipitously, suggesting a lack of demand.

That points to dollar strength compared to the currencies of our trading partners.

The U.S. economy, and more to the point consumer spending, was kept afloat during the pandemic by federal income assistance programs. Now, the economy is benefiting from a strong dose of infrastructure spending.

What’s more, the economy has yet to reap the full benefits of industrial policies. These policies, once out of favor, are financing the onshore production of semiconductor chips, electric vehicles and solar panels in addition to the tech hubs across the continent.

Read more of RSM’s insights on the dollar, the economy and the middle market.

We expect that the expansion of domestic high-value production capabilities will continue to attract foreign capital into what looks to be a U.S. economic renaissance.

While the U.S. has put its industrial policy programs in place, the European Union finds itself playing catchup.

Economic activity in Europe has been battered by Russia’s war on Ukraine and by competition from the cheaper goods produced by China.

Europe’s recent steps suggest that this new era of industrial policy is becoming more acceptable among the democracies in the West. The trend is likely to continue as the West comes to terms with China’s practices of dumping and market cornering.

While the politics in the U.S. seem up in the air, it seems most likely that whatever the outcome of the election, there will be increased fiscal spending.

Another factor is that half of the U.S. budget goes to defense. And with the necessity of countering Russia’s war aspirations in Europe and China’s threatening posture toward Taiwan and the Philippines, there is the likelihood of higher U.S. defense spending, which will most likely retain strength in the dollar.

Just as the dollar moved higher during the Reagan years in the 1980s, the dollar has moved higher today because of defense spending at the height of the Cold War.

In fact, the dollar reached its peak in 1985, when the Federal Reserve’s chairman at the time, Paul Volcker, raised the federal funds rate to 18%, the penultimate example of a tight monetary policy working in conjunction with an expansionary fiscal policy to increase the value of a currency.

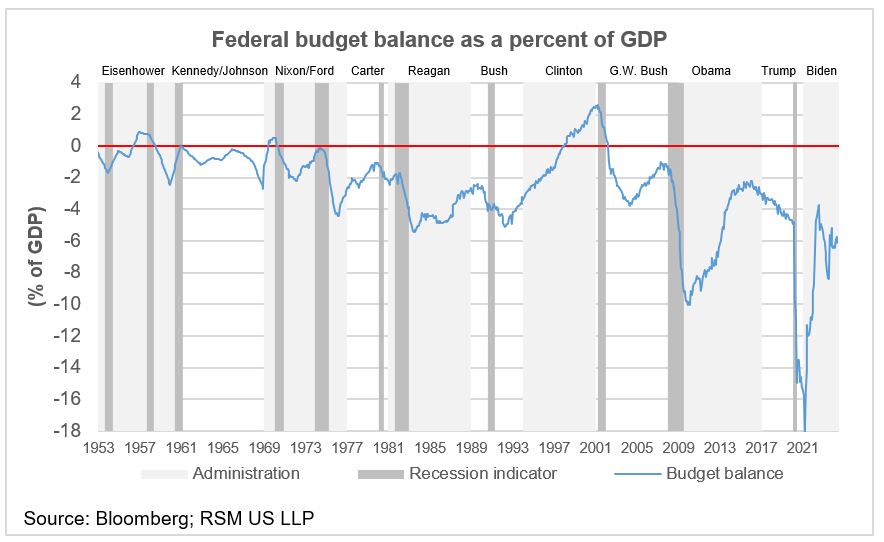

Since the 1980s, the federal budget deficit has been greater than 5% only twice, after the financial crisis and during the pandemic.

While the end of pandemic income assistance and the economic recovery are working to reduce the federal budget deficit, that leaves room for increased military spending should the geopolitical situation deteriorate further.

The takeaway

A strong dollar has its benefits and drawbacks. On the plus side, a strong dollar helps dampen U.S. inflation as consumers pay less for foreign-made goods.

On the negative side, U.S. exports, which comprise about 11% of gross domestic product, become more expensive. This in turn creates a drop in foreign demand that becomes a drag on U.S. GDP growth.

Another drawback is that a strong dollar and higher interest rates, in attracting capital to the U.S., can strain emerging markets with weak balance sheets and fiscal imbalances.

The dollar’s strength is unlikely to diminish anytime soon. The notion of a coordinated currency intervention by the democracies in the West is pure folly; it’s an expensive way for a country to spend its currency reserves.

Just like the price of oil, the value of the dollar is set by the forces of supply and demand. At the moment, the demand for the dollar and dollar-denominated assets outweighs the demand for currencies of our trading partners in the West.

The dollar is backed by the power and stability of the U.S. monetary authorities and its financial markets and their ability to determine the course of economic growth.

At the moment, investment by the U.S. corporate sector, in partnership with the U.S. government, is propelling the U.S. economy, forming the macroeconomic and financial forces supporting the dollar.

{kind=link}