The United Kingdom stock market has shown robust performance recently, with a 1.7% increase over the past week and an 8.9% rise over the last year, alongside expectations of a 13% annual earnings growth. In this context, companies with high insider ownership can be particularly compelling as they often indicate a strong alignment between management’s interests and those of shareholders.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

|

Name |

Insider Ownership |

Earnings Growth |

|

Plant Health Care (AIM:PHC) |

26.4% |

121.3% |

|

Getech Group (AIM:GTC) |

17.3% |

108.7% |

|

Petrofac (LSE:PFC) |

16.6% |

124.5% |

|

Gulf Keystone Petroleum (LSE:GKP) |

10.8% |

47.6% |

|

Integrated Diagnostics Holdings (LSE:IDHC) |

26.7% |

25.5% |

|

LSL Property Services (LSE:LSL) |

10.8% |

33.3% |

|

Velocity Composites (AIM:VEL) |

28.5% |

143.4% |

|

TEAM (AIM:TEAM) |

25.8% |

58.6% |

|

Afentra (AIM:AET) |

38.3% |

64.4% |

|

Mothercare (AIM:MTC) |

15.1% |

41.2% |

We’re going to check out a few of the best picks from our screener tool.

Simply Wall St Growth Rating: ★★★★☆☆

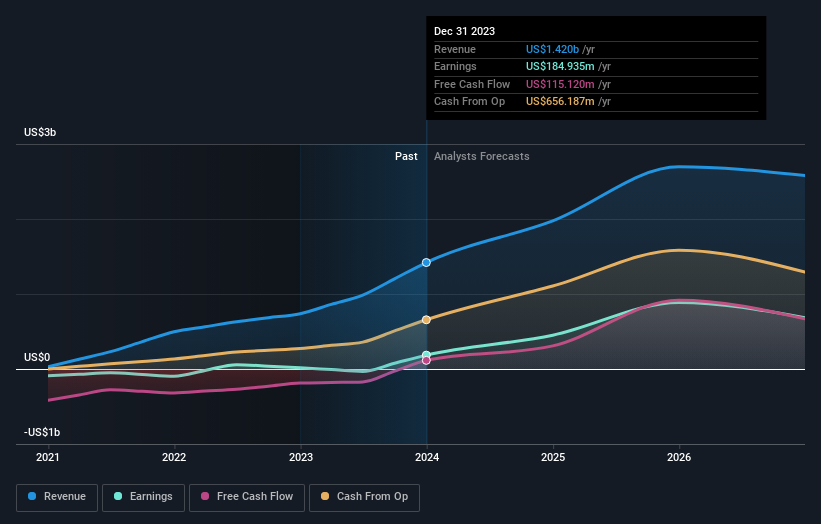

Overview: Energean plc is a company focused on the exploration, development, and production of oil and gas, with a market capitalization of approximately £1.91 billion.

Operations: The company generates its revenue primarily from the exploration and production of oil and gas, totaling approximately $1.42 billion.

Insider Ownership: 10.7%

Earnings Growth Forecast: 18.3% p.a.

Energean, a growth-oriented company with significant insider ownership, is trading at 40.7% below its estimated fair value, suggesting potential undervaluation. Despite high debt levels and recent shareholder dilution, Energean has demonstrated robust performance with earnings growth of 970.8% over the past year. Analysts expect both revenue and earnings to outpace the UK market average significantly in the coming years. However, its dividend coverage remains weak, reflecting challenges in sustaining payouts amidst rapid expansion.

Simply Wall St Growth Rating: ★★★★★☆

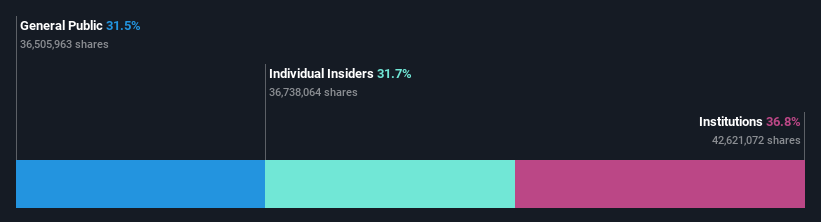

Overview: Foresight Group Holdings Limited is a UK-based infrastructure and private equity manager with operations in Italy, Luxembourg, Ireland, Spain, and Australia, boasting a market capitalization of approximately £576.47 million.

Operations: The company generates revenue through three primary segments: Infrastructure (£85.68 million), Private Equity (£39.28 million), and Foresight Capital Management (£11.33 million).

Insider Ownership: 31.7%

Earnings Growth Forecast: 30.9% p.a.

Foresight Group Holdings, a UK-based growth company with high insider ownership, is trading at 32.8% below its estimated fair value, indicating potential undervaluation. While the firm’s profit margins have declined from last year to 15.4%, it boasts a forecasted earnings growth of 30.9% annually and revenue growth of 10% per year, both surpassing UK market averages. However, its dividend coverage is weak at 4.46%, suggesting challenges in sustaining payouts despite robust growth projections and a very high expected Return on Equity of 41.5%.

Simply Wall St Growth Rating: ★★★★☆☆

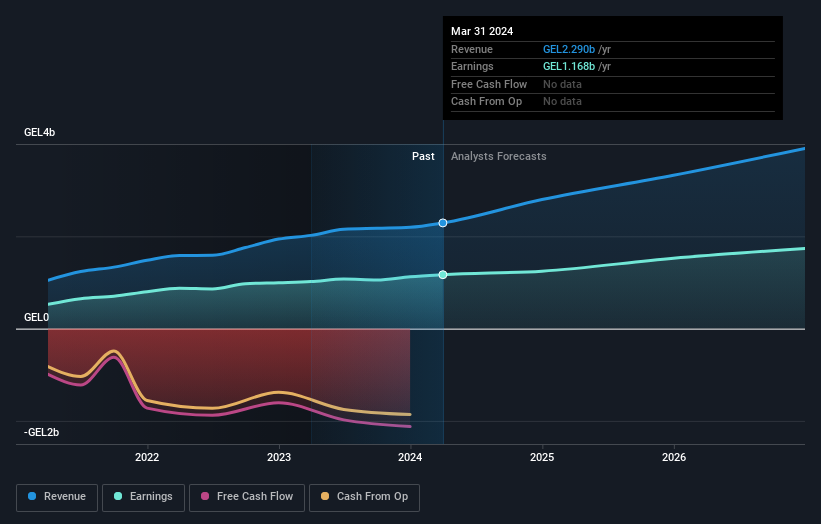

Overview: TBC Bank Group PLC operates in Georgia, Azerbaijan, and Uzbekistan, offering a range of services including banking, leasing, insurance, brokerage, and card processing to both corporate and individual clients with a market capitalization of approximately £1.38 billion.

Operations: The company generates revenue through diverse financial services such as banking, leasing, insurance, brokerage, and card processing in Georgia, Azerbaijan, and Uzbekistan.

Insider Ownership: 18%

Earnings Growth Forecast: 15.2% p.a.

TBC Bank Group, amidst a volatile share price, has shown robust financial performance with earnings growing by 23.6% annually over the past five years. It’s trading at 47.7% below its estimated fair value, suggesting potential undervaluation relative to peers. Recent strategic moves include a GEL 75 million share buyback to enhance shareholder value and strong Q1 results with significant increases in net interest income and net income from the previous year, reinforcing its growth trajectory despite some concerns over high bad loans at 2.1%.

Make It Happen

Interested In Other Possibilities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include LSE:ENOG LSE:FSG and LSE:TBCG.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

{kind=link}